The global industrial landscape is witnessing a significant transformation, with carbon black emerging as a critical component in various high growth sectors. Primarily known for its role as a reinforcing filler in tires, carbon black’s utility has expanded far beyond the automotive industry. Today, it is an essential material in the production of plastics, high performance coatings, and advanced electronics. As manufacturing processes become more sophisticated, the demand for specialized grades of carbon black engineered for specific conductivity, UV protection, and pigmentation is surging globally.

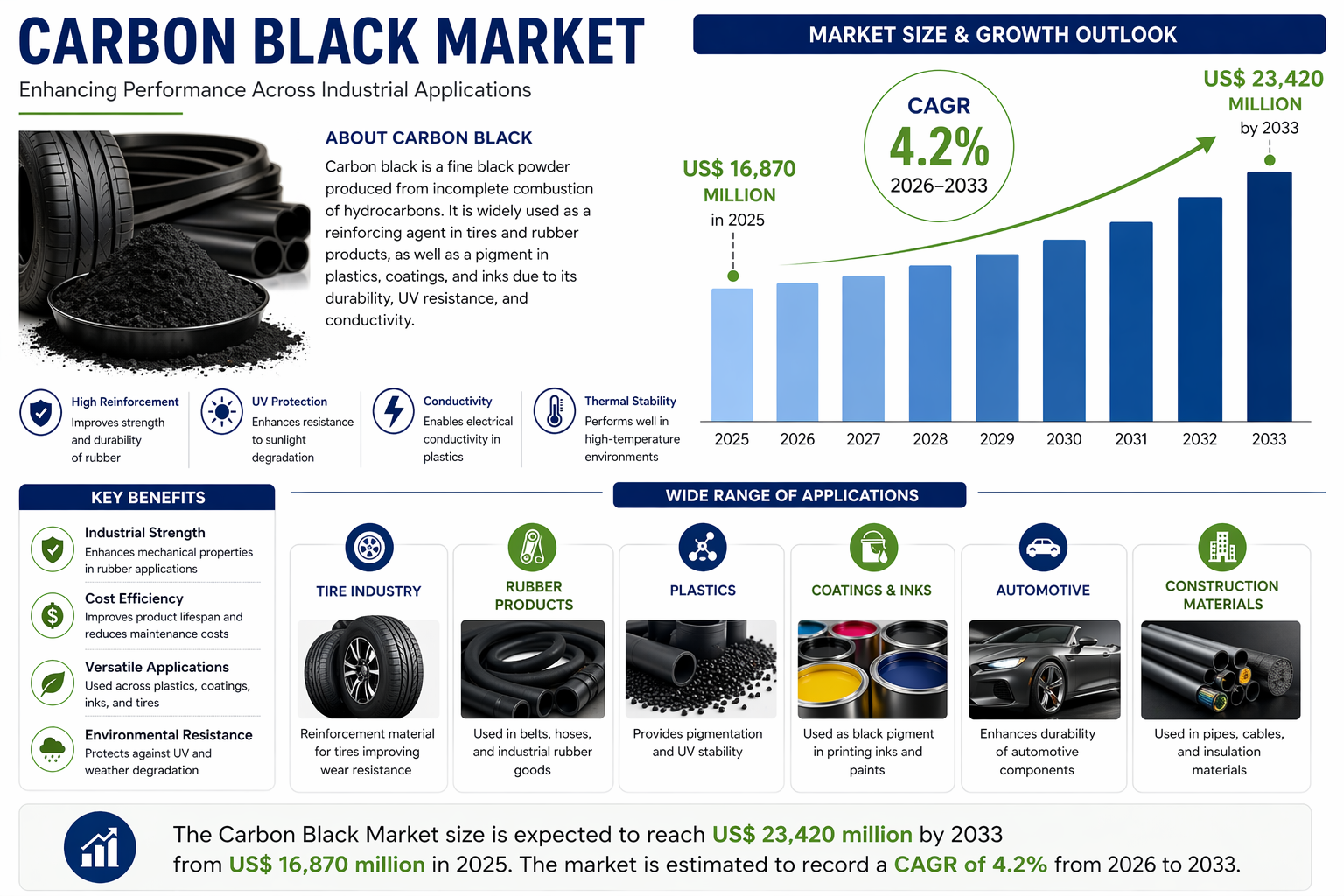

The Carbon Black Market size is expected to reach US$ 23,420 million by 2033 from US$ 16,870 million in 2025. The market is estimated to record a CAGR of 4.2% from 2026 to 2033. This steady growth trajectory is fueled by the rapid expansion of the electric vehicle (EV) market, the industrialization of emerging economies, and continuous innovations in material science that allow carbon black to meet more stringent performance standards.

Carbon Black Market Trends and Drivers and Opportunities

The growth of the carbon black industry is governed by a complex interplay of industrial needs and environmental regulations. A primary driver is the robust growth of the global automotive sector, particularly in the Asia-Pacific region. As vehicle production increases, so does the demand for durable, high-performance tires. Carbon black is indispensable in this regard, as it improves the tensile strength and wear resistance of rubber. Furthermore, the shift toward Electric Vehicles (EVs) is creating a unique opportunity. EVs require tires with lower rolling resistance to preserve battery life and high-conductivity materials for battery electrodes, both of which are high-value applications for specialty carbon black.

Another significant trend is the rising demand for "Specialty Carbon Black." Unlike standard furnace black, specialty grades are utilized in the plastics and coatings industries to provide UV protection, chemical resistance, and deep black aesthetics. In the packaging industry, carbon black is increasingly used to produce conductive packaging for sensitive electronic components.

Sustainability has also become a major market driver. The industry is pivoting toward "Recovered Carbon Black" (rCB), which is derived from the pyrolysis of end-of-life tires. This circular economy approach addresses environmental concerns regarding tire waste while providing a sustainable raw material source for manufacturers. Companies that invest in green manufacturing technologies and bio-based feedstocks are expected to gain a competitive edge in the coming decade.

Download Sample PDF Report: https://www.businessmarketinsights.com/sample/BMIPUB00033808

Strategic Market Segmentation

The market is categorized based on type, application, and geography. By type, the market includes furnace black, channel black, thermal black, and acetylene black. Furnace black remains the dominant segment due to its versatile application in tire manufacturing. In terms of application, the tire industry holds the largest market share, followed by non-tire rubber goods, plastics, inks, and coatings.

Geographically, Asia-Pacific leads the market, driven by the massive manufacturing hubs in China and India. The region benefits from lower production costs and a high concentration of automotive OEMs. However, North America and Europe are seeing a shift toward premium specialty grades driven by strict environmental regulations and the presence of advanced aerospace and healthcare industries.

Competitive Landscape and Top Players

The global carbon black market is highly competitive, with key players focusing on capacity expansion, mergers, and sustainable product development. The leading companies are investing heavily in R&D to produce low-PAH (Polycyclic Aromatic Hydrocarbons) carbon black to comply with tightening safety regulations in the EU and North America.

The top players in the market include:

-

Cabot Corporation

-

Birla Carbon (Aditya Birla Group)

-

Orion Engineered Carbons

-

Tokai Carbon Co., Ltd.

-

Mitsubishi Chemical Corporation

-

Jiangxi Black Cat Carbon Black Inc., Ltd.

-

China Synthetic Rubber Corporation (CSRC)

-

Omsk Carbon Group

-

Phillips Carbon Black Limited (PCBL)

Future Outlook: Path to 2033

Looking toward 2033, the market will likely be defined by "smart" and "green" carbon black. As the world moves toward decarbonization, manufacturers are under pressure to reduce the carbon footprint of the production process itself. The integration of digitalization in manufacturing (Industry 4.0) will allow companies to optimize feedstock usage and reduce emissions. Additionally, the expansion of the electronics sector—specifically in conductive polymers for 5G infrastructure and wearable technology—presents a lucrative frontier for market participants.

About Us

Business Market Insights is a one-stop-shop for tiered market research reports that include deep-dive analysis of various industry verticals. We provide comprehensive data regarding market size, share, growth drivers, and challenges to help stakeholders make informed decisions. Our research methodology is designed to provide high-quality, accurate, and actionable insights.

Contact us:

Phone: +1-646-491-9876

Email: sales@businessmarketinsights.com