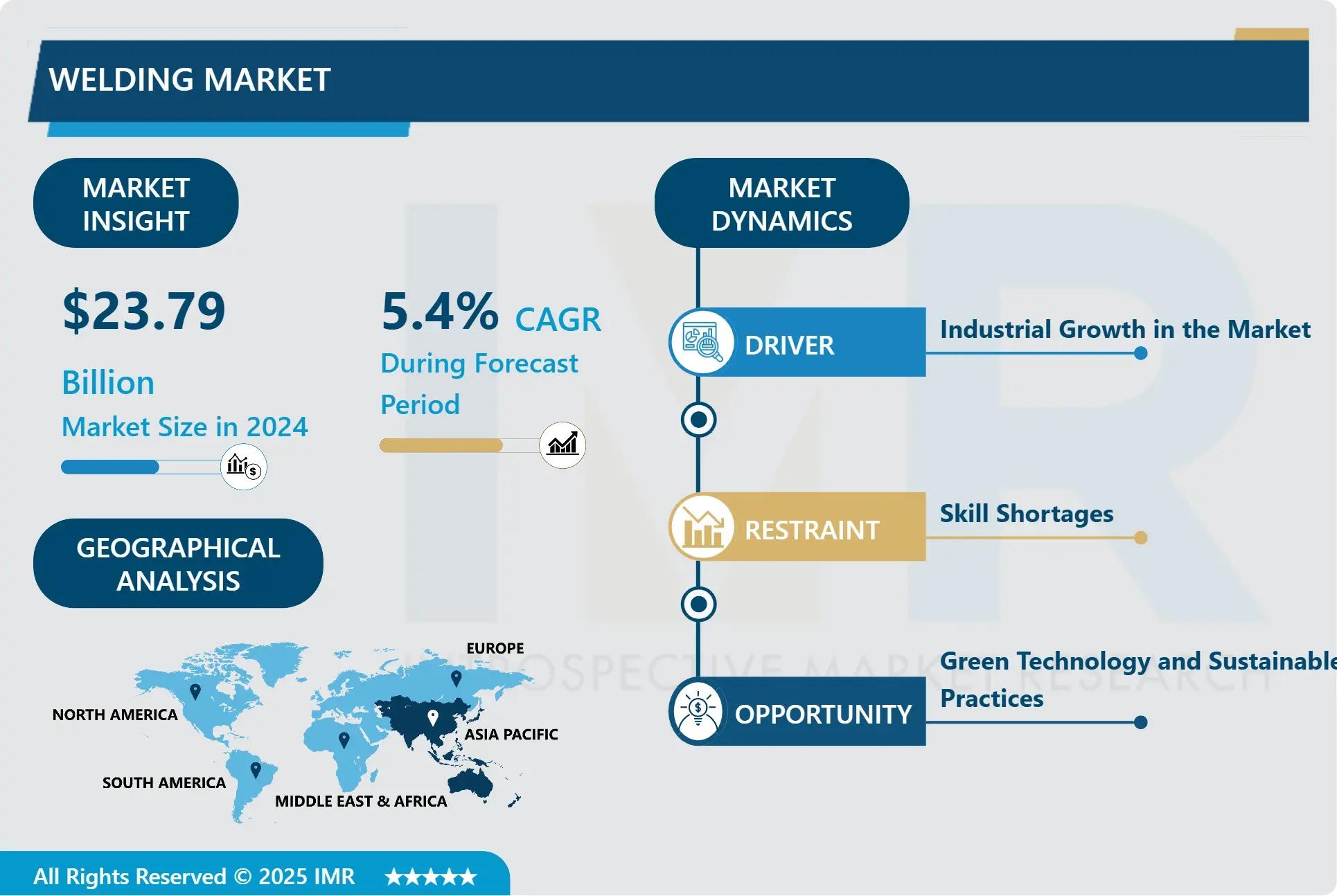

According to a new report published by Introspective Market Research, Welding Market by Technology, Equipment, End-User, and Region, The Global Welding Market Was Valued at USD 23.79 Billion in 2024 and is Projected to Reach USD 36.23 Billion by 2032, Growing at a CAGR of 5.4%.

Market Overview:

The global Welding market encompasses the equipment, consumables, and services used to join materials, primarily metals and thermoplastics, through coalescence. This includes technologies such as arc welding, resistance welding, laser beam welding, and solid-state welding, along with associated consumables like electrodes, filler metals, and shielding gases. Modern welding solutions offer significant advantages over traditional joining methods like riveting or bolting, including superior joint strength, design flexibility, material efficiency, and the ability to create seamless, leak-proof connections. Advanced automated and robotic systems further enhance precision, productivity, and workplace safety.

Growth Driver:

The primary growth driver for the welding market is the sustained global investment in infrastructure development and the expansion of the manufacturing sector, particularly in transportation and energy. Massive government initiatives for roads, bridges, railways, and urban development worldwide create continuous demand for welding in structural steelwork. Simultaneously, the booming automotive industry, especially with the shift towards electric vehicles (EVs) requiring specialized battery tray and chassis welding, and the shipbuilding sector drive significant consumption of welding equipment and consumables. Furthermore, investments in energy infrastructure including traditional oil & gas pipelines and new renewable energy projects like offshore wind farms and solar panel structures rely heavily on advanced welding techniques, ensuring robust, long-term demand across multiple, high-volume industrial sectors.

Market Opportunity:

A significant and high-growth market opportunity lies in the adoption of automation, robotics, and digitalization within welding processes. The transition from manual welding to automated robotic cells, especially for high-volume, repetitive tasks in automotive and manufacturing, offers substantial gains in precision, quality consistency, and productivity while addressing skilled labor shortages. Furthermore, the integration of Industry 4.0 technologies—such as IoT sensors for real-time weld monitoring, AI-driven quality control, and cloud-based data analytics for predictive maintenance and process optimization—creates a new frontier for value-added services. Developing and providing these smart welding solutions, including collaborative robots (cobots) for small-batch fabrication, allows companies to capture premium market segments and build deeper partnerships with manufacturers seeking to modernize their production floors.

Welding Market, Segmentation

The Welding Market is segmented on the basis of Technology, Equipment, and End-User.

Technology

The Technology segment is further classified into Arc Welding, Resistance Welding, Laser Beam Welding, Ultrasonic Welding, and Others. Among these, the Arc Welding sub-segment accounted for the highest market share in 2024. Arc welding, including processes like shielded metal arc welding (SMAW), gas metal arc welding (GMAW/MIG), and gas tungsten arc welding (GTAW/TIG), dominates due to its versatility, relatively low equipment cost, and widespread applicability across construction, fabrication, and repair & maintenance activities. Its ability to weld a vast range of materials and thicknesses makes it the most universally adopted welding technology globally.

End-User

The End-User segment is further classified into Automotive, Construction, Shipbuilding, Energy & Power, Heavy Machinery, and Others. Among these, the Automotive end-user segment accounted for the highest market share in 2024. The automotive industry is the largest consumer, driven by high production volumes and the intensive use of welding in body-in-white (BIW) assembly, chassis fabrication, and component manufacturing. The shift towards electric vehicles is further stimulating demand for new welding techniques suitable for aluminum and high-strength steel, cementing this sector's leading position.

Some of The Leading/Active Market Players Are-

• Lincoln Electric Holdings, Inc. (USA)

• Illinois Tool Works Inc. (USA)

• Colfax Corporation (ESAB) (USA)

• Air Liquide S.A. (France)

• Kemppi Oy (Finland)

• Fronius International GmbH (Austria)

• Obara Corporation (Japan)

• Panasonic Holdings Corporation (Japan)

• Amada Weld Tech Co., Ltd. (Japan)

• Daihen Corporation (Japan)

• Miller Electric Mfg. LLC (USA)

• Hobart Brothers (USA)

• voestalpine Böhler Welding (Austria)

• Arcon Welding Equipment (USA)

• Rofin-Sinar Technologies Inc. (Germany)

• and other active players.

Key Industry Developments

News 1:

In March 2024, Lincoln Electric launched its new "VeloX™" robotic welding cell integrated with AI-powered vision software. The system automatically identifies weld seams and adjusts parameters in real-time, targeting the high-mix, low-volume manufacturing segment with a solution that reduces programming time and improves first-pass weld quality.

News 2:

In January 2024, Fronius introduced a next-generation digital welding platform that connects all shop floor welding machines to a central cloud analytics dashboard. This provides manufacturers with real-time data on energy consumption, consumable usage, and arc-on time for optimizing production efficiency and predictive maintenance scheduling.

Key Findings of the Study

• Arc Welding is the dominant technology due to its versatility and cost-effectiveness across industries.

• The Asia-Pacific region leads the market, fueled by massive manufacturing and infrastructure activity.

• Global infrastructure development and expansion in automotive and energy sectors are key growth drivers.

• Major trends include rapid adoption of automation/robotic welding and digitalization with IoT and AI for smart, data-driven welding solutions.