A fundamental philosophical and architectural shift is at the very core of the global Secure Access Services Edge Market: the enterprise-wide adoption of a "Zero Trust" security model. For decades, corporate security was based on a flawed, perimeter-centric model of "trust but verify." If a user was "inside" the corporate network, they were implicitly trusted and often given broad access to a wide range of applications and data. This created a massive security vulnerability. A single compromised user credential could give an attacker a free pass to move laterally across the entire network. The Zero Trust model, as its name implies, completely inverts this. It operates on the simple but powerful principle of "never trust, always verify." In a Zero Trust architecture, no user, device, or application is trusted by default, regardless of its location. Every single access request to a resource is treated as a new, untrusted connection that must be explicitly and continuously verified based on a combination of factors, including the identity of the user, the health and security posture of their device, the application being accessed, and other contextual signals. This granular, identity-centric approach to security dramatically reduces the attack surface and is a far more effective model for the modern, distributed, work-from-anywhere world. The SASE architecture is the primary delivery vehicle for implementing a Zero Trust strategy at scale.

Market Key Players

The key players who have most successfully built their platforms around the Zero Trust philosophy are the leaders in the Security Service Edge (SSE) component of the SASE market. Zscaler is a key player and a pioneer in this space. Its entire platform is built on the concept of a "Zero Trust Exchange," which acts as an intelligent switchboard, connecting users directly to applications without ever placing them on the corporate network. Netskope is another key player, with a strong, data-centric approach to Zero Trust, focusing on providing deep visibility and granular control over data in the cloud. Palo Alto Networks is a major key player, having evolved its next-generation firewall capabilities into a comprehensive Zero Trust platform with its Prisma Access SASE offering. The major identity and access management (IAM) providers, such as Okta and Microsoft (with its Entra ID platform), are also crucial key players in the Zero Trust ecosystem, as they provide the foundational identity and authentication services upon which the entire model is built. The successful implementation of Zero Trust requires a deep integration between the SASE platform and the organization's chosen identity provider.

Market Segmentation

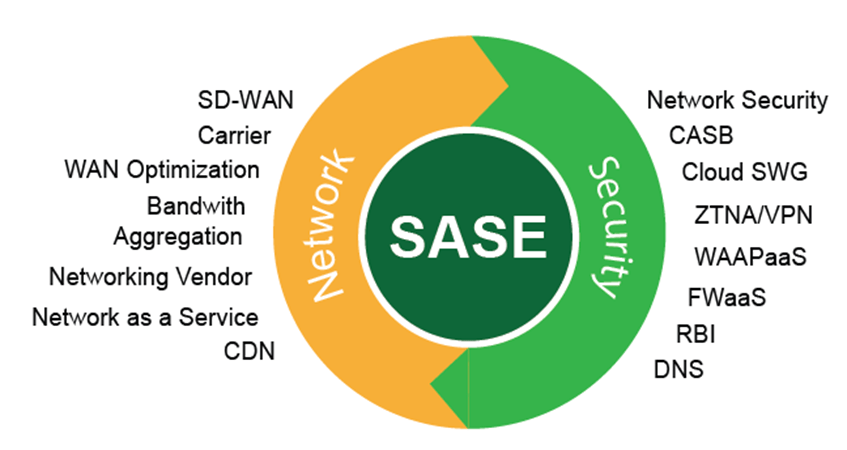

The Zero Trust trend creates a key segmentation within the SASE market based on the specific capabilities offered. The first and most critical segment is Zero Trust Network Access (ZTNA). This is the core technology that replaces the traditional VPN. ZTNA provides secure, identity-based access to private applications hosted in a data center or a public cloud. It is a massive and rapidly growing segment as companies look to decommission their insecure and clunky VPN infrastructure. The second segment involves applying Zero Trust principles to internet and SaaS access. This is the role of the Secure Web Gateway (SWG) and Cloud Access Security Broker (CASB) components of the SSE stack. These tools ensure that all user traffic to the public internet and to SaaS applications is inspected for threats and that corporate data security policies are enforced. The third segment is Zero Trust for the network itself, through the use of micro-segmentation technologies that can prevent the lateral movement of an attacker within a network, even after an initial breach has occurred. A comprehensive SASE platform must provide strong capabilities across all these segments to deliver on the full promise of Zero Trust.

Market Region & Market Trends

The adoption of Zero Trust is a global trend, but its urgency and implementation focus vary by region. In North America, adoption has been strongly driven by a series of high-profile data breaches and a federal government mandate requiring all US federal agencies to move to a Zero Trust architecture. This has created a massive and well-defined market. In Europe, the adoption of Zero Trust is heavily influenced by the need to comply with GDPR, with a strong focus on using the "least privilege" access principles of Zero Trust to protect personal data. In the APAC region, the adoption is more nascent but is accelerating rapidly as businesses in the region undergo rapid digital transformation and cloud adoption. A key global trend for the future is the extension of the Zero Trust model beyond human users to also secure the growing number of non-human entities, such as IoT devices and service-to-service API communications. The future is about applying the "never trust, always verify" principle to every single connection on the network. The Secure Access Services Edge Market is projected to grow to USD 42.86 Billion by 2035, exhibiting a CAGR of 22.1% during the forecast period 2025-2035.

Most Popular Market Research Reports:

Canada Body Worn Camera Market

Germany Sports Analytics Market