Here's something I see consistently working with payment operations teams: merchants losing 8 to 15% of their revenue not because customers changed their minds, but because their payment infrastructure failed them at the wrong moment.

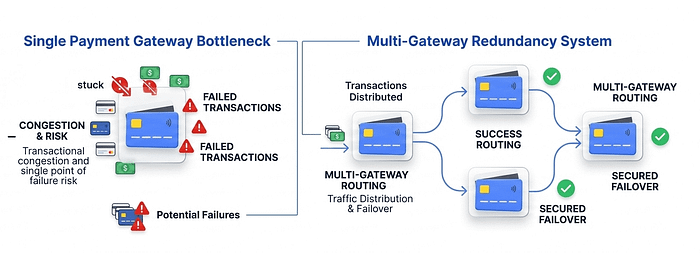

A single gateway goes down during a flash sale. A processor flagging a batch of legitimate transactions. A regional bank declined cards from a specific BIN range. These aren't edge cases. They happen every week, and if your entire revenue stream runs through one gateway, every one of these events hits your bottom line directly.

Running multiple payment gateways is how serious merchants protect authorization rates, reduce single points of failure, and build infrastructure that scales. Here's what that actually looks like in practice.

What Multiple Payment Gateways Really Mean

A multiple payment gateway setup means routing across transactions two or more payment processors, rather than relying on a single provider for every sale.

In its simple form, it means having a backup. In a more mature implementation, it means intelligent routing, where your system decides in real time which gateway gives each transaction the best chance of approval, based on card type, geography, issuer behavior, and historical performance data.

According to Google Cloud’s financial services solutions, building resilient payment architectures with multi-region redundancy across zones is essential for scaling high-availability commerce systems. It’s not a luxury configuration. It’s infrastructure design.

The Approval Rate Problem No One Talks About Openly

Here’s what most merchants don’t track: the difference in approval rates between gateways for the same card types.

I’ve seen merchants running the same transaction profile through two gateways and finding approval rate gaps of 6 to 12 percentage points, depending on the issuer and card scheme. That gap represents real revenue. It compounds daily.

A 2024 Forrester report on payment optimization found that merchants who implemented intelligent gateway routing saw average authorization rate improvements of 7%, with the highest gains coming from international and cross-border transactions. When you consider that most high-volume merchants are processing thousands of transactions daily, a 7% improvement in authorization isn’t incremental. It’s transformational.

This is why approval rate analysis needs to happen at the gateway level, not just the account level. If you’re only looking at aggregate decline rates, you’re missing where the problem actually lives.

Multiple Payment Options Are a Customer Expectation Now

Beyond infrastructure resilience, there’s a conversion angle that often gets overlooked.

Baymard Institute research indicates that 13% of customers abandon checkout when a preferred payment method isn’t available. Customers in Southeast Asia expect different payment rails than customers in Germany. A customer using a Visa prepaid card has different approval dynamics than someone using a corporate Mastercard.

Having multiple payment options supported at checkout, backed by the right gateway for each payment type, is how you meet customers where they are instead of forcing them into your infrastructure constraints.

How to Integrate Multiple Payment Gateways Without Creating Chaos

The technical side of multiple payment gateway integration is manageable if you approach it with a clear routing logic framework from the start.

The core components you need are:

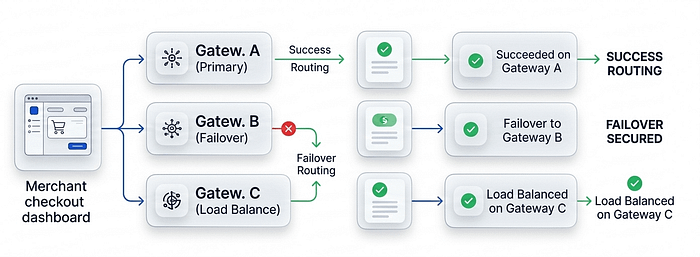

Gateway selection logic. This is the decision layer that routes each transaction based on real-time and historical signals: card BIN data, issuer country, transaction amount, payment method, and gateway-specific approval rate history. If you’re not leveraging BIN data in your routing decisions, you’re routing blind.

Failover handling. When a gateway returns a decline or a technical error, your system needs to know whether to retry on the same gateway or reroute immediately. This is where payment retry strategies matter enormously. A smart retry on an alternate gateway recovers revenue. A dumb retry on the same gateway that already declined just burns customer goodwill.

Compliance and monitoring per gateway. Each gateway relationship comes with its own rules, chargeback thresholds, and compliance requirements. Running multiple gateways means you need to track card scheme compliance and monitoring across all of them simultaneously. The Visa Acquirer Monitoring Program has different thresholds that apply per merchant ID, and if one gateway’s MID crosses a threshold while you’re not watching, the consequences fall on you.

Fraud signal sharing. Running gateways in silos means your fraud detection is also siloed. A transaction that gets flagged on one gateway might slide through another. If you’re not building 3D Secure authentication and fraud signals into a unified view, you’re creating gaps that bad actors will find.

If you want help mapping out a routing architecture that fits your transaction mix, talk to our team. We work specifically with high-risk and high-volume merchants on this.

The Chargeback Risk of Getting This Wrong

There’s a risk in multiple gateway setups that most implementation guides don’t mention: chargeback liability gets distributed across multiple MIDs, which can obscure your true dispute rate until you’re already in trouble.

Academic research from the Federal Reserve’s payment systems division has documented how merchants operating across multiple processor relationships frequently underestimate aggregate chargeback exposure because monitoring is fragmented by gateway.

If you’re scaling a multiple gateway setup, you need unified chargeback visibility from day one. That means tracking disputes at the customer level, not just the gateway level, and having chargeback alert systems that pull from all your processing relationships. A single customer who files friendly fraud claims across two different gateways can hit your business twice before any system flags the pattern.

For merchants already seeing dispute volume climb, see how we approach chargeback prevention before it becomes a monitoring program issue.

The Revenue Impact Is Measurable

The financial case for multiple payment gateway integration isn’t theoretical. It comes down to three numbers:

Your current authorization rate. Your current failover recovery rate (often zero if you have one gateway). And your average order value multiplied by daily transaction volume.

If you're processing $500,000 per month with a 90% authorization rate and a single gateway, a 5% improvement in auth rate from intelligent routing is $25,000 per month in recovery revenue. That's a payback period measured in days, not quarters.

Failed payments that aren't recovered also drive involuntary churn , especially for subscription businesses. A customer whose card declines and never gets a recovery attempt doesn't always come back. Routing to an alternate gateway in real time is the cleanest form of failed payment recovery available.

Where to Start

If you're running a single gateway today, the immediate priority is standing up at least one alternative processor with failover routing. That alone eliminates your single point of failure.

If you're already on two gateways but routing is manual or rule-based, the next step is implementing performance-based routing that uses real approval rate data by card type and issuer to make routing decisions dynamically.

If you're operating at scale and want to optimize across multiple gateways simultaneously, that's where payment routing becomes a real competitive advantage, and where the architecture decisions you make today determine your revenue ceiling tomorrow.

If you're not sure where your current setup is losing revenue, let's look at it together . A routing audit usually surfaces the biggest opportunities within the first session.